TVM 2$days

TVM Tuesdays is a weekly blog that offers a fun, new take on this age-old topic and financial education insights from Brent Pritchard.

Sign up for email notifications:

TVM Rules.

They matter. And yes, it does!

Word of mouth is still and will always be the best form of marketing. (Even a finance instructor knows that!) Will you please help us spread the word about our YouTube channel, TVM Rules, and the book, also known as the “Boomerang book,” that made it possible?

Here’s an excerpt from my book Would Your Boomerang Return? What Birds, Hurdlers, and Boomerangs Can Teach Us About the Time Value of Money (2023):

You’ve likely purchased—and had delivered to your house—one or more products that came with parts to assemble, a user manual, and a simple tool. Have you ever had the unfortunate circumstance of opening a box only to find that one or more pieces are missing? It happens from time to time and crushes your ambition. But presumably every one of the user manuals you’ve ever handled has provided all the important or essential information needed. Many user manuals include multiple languages. In this case, the first thing you need to do is locate your language. What good are instructions if the words don’t make sense? While some are far easier to read than others, there aren’t many user manuals out there that require you to go elsewhere because they are incomplete. A company selling a product that repeatedly didn’t include in the box all the pieces that would allow the owner to use the item, including a complete manual and the simple tool, would no doubt get bad reviews and wouldn’t likely be in business for long.

I wouldn’t expect you to think otherwise, yet that’s exactly what I’d found in the market with respect to the content related to the Time Value of Money! The product in the box, more precisely the Time Value of Money content within these other books, was missing pieces of information.

Now I’m a pretty practical guy with a good amount of common sense or street smarts. Having worked in industry, I know that quality work product requires adherence to a certain standard of excellence. This is why restaurants have to dish out good food to stay open for business. Word of mouth is still and will always be the best form of marketing or anti-marketing. So it’s beyond me how these other providers of content on the topic of the Time Value of Money can continue to dish out a product that leaves people with a bad taste in their mouths.

What would it take for you to like our videos, subscribe to our YouTube channel, or tell a friend (maybe even a child-friend) about TVM Rules? What if I told you that your support will ultimately help aspiring and current finance professionals and finance educators?

(I know it takes time, but it’s about time aspiring and current finance professionals had an effective tool for applying the Mathematics of Finance to analyze and evaluate real-world Time Value of Money situations—in the classroom, in practice, or while sitting for an industry designation examination. They’ll thank you, and we thank you for your consideration and support!)

https://www.youtube.com/@TimeValueofMoneyRules

Let the spreading or sharing begin!

Brent Pritchard is an author and college finance lecturer with over two decades of industry experience and cofounder of Boxholm Press, LLC, a family-owned-and-operated publishing company providing educational content, products, and services. He pioneers an innovative and approachable new way of learning and teaching the Time Value of Money as well as thought leadership in other business topics. His most recent book is Would Your Boomerang Return? You can contact him on his website here.

Now 312 Is More Than Chicago’s Area Code!

My wife, Sarah, and I are both teachers. Just the other day, we were talking about how nice it is to have the flexibility to choose when we want to work in the office. (Yes, teachers do work in the summer months.) The conversation was timely. Before too long, I’d be sitting down to write the week’s post which is about time.

When you’re analyzing a real-world Time Value of Money situation, here’s how it’s going to go down:

Either you’ll have the flexibility to choose which investment yield to use or not. (See TVM Rule #3.)

Regardless of whether you have such flexibility, you will need to determine whether you can use the stated yield or rate. It’s that simple. How do we know whether we’ll have the luxury of choice or flexibility? Enter the 312 “warm-up” routine.

Here’s an excerpt from my book Would Your Boomerang Return? What Birds, Hurdlers, and Boomerangs Can Teach Us About the Time Value of Money (2023):

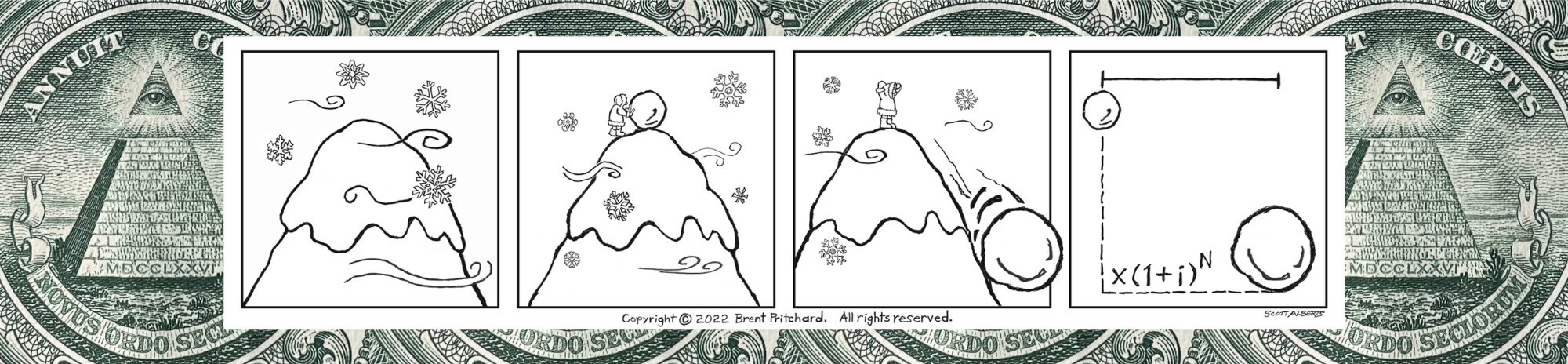

…it takes 3 and 1 to get to 2. First you count money, next you tell time, and then you can “read and write” the true investment yield. You’ll find an entire chapter in this user manual on the topic of reading and writing “i,” which is the ultimate goal of the 312 warm-up routine.

I’ve written about the TVM Rules before. They’re important. This probably won’t be the last time I write about them. You can remember the TVM Rules with one word: indifferent. Why would you want to remember the TVM Rules? Because they were developed around the mnemonic and audible aid indifferent that helps you determine the appropriate true investment yield. Without it don’t even bother trying to work out the math.

Let’s take a look at a few words from the rearranged TVM Rules:

3. …different payment types and signs.

1. …in different points in time.

2. …correspond the time span in between periods or payments (on the timeline) and the time span of the true investment yield.

The point of the 312 warm-up routine is to determine or calculate the “i” you’ll need to apply the Mathematics of Finance as described in TVM Rule #2. But before we can do that we must cycle through the mnemonic and audible aid indifferent in a 3-1-2 manner.

First TVM Rule #3. What is the p(ay)m(en)t? In other words, a PMT or payment (PV or FV)? In further words, an even annuity or a single payment? And then you’re on to TVM Rule #1 just like that. If you’re dealing with an annuity you don’t have the flexibility to choose how you’re going to tell time. You have to use the true investment yield that matches the timing of the frequent payments.

For the real-world situations that follow, let’s say you were given a true annual investment yield of 7.7633% with monthly compounding. (Because all interest rates are expressed in annual terms right?!)

First, let’s say you’re asked to determine the future value in one year of $100 to be received today. You have the flexibility to choose which investment yield to use because you’re dealing with a lump-sum payment. If you wanted to tell time in annual terms, then you’d have your “i.” In other words, you can use the stated (true annual investment) yield. Remember, a true investment yield considers the effects of compounding! (And for the record, even if there’s no compounding during the time span of the true investment yield in the case of a true annual investment yield with annual compounding it still considers (the effects of) compounding.)

Now on to the second real-world example that considers an even annuity which contemplates monthly deposits of $100 for one year starting one month from now. In other words, the payment is frequent and level in terms of amount and timing. So, you’re using the PMT key on your financial calculator. In this example, you don’t have the flexibility to choose which investment yield to use because you’re dealing with an annuity. You’re being told how to tell time. But you still need to determine whether you can use the stated yield or rate. In this situation, only a true monthly investment yield will work. (The answer is 0.625% if you were curious.)

I’ve written about how to manipulate yields in the book and blog. That’s the point of the 312 warm-up routine, but it’s not the main point of this post which is to show you the significance and flexibility of the mnemonic and audible aid indifferent.

What true investment yield could you use for the first real-world example that considers a single payment if you were telling time with a monthly, quarterly, or semiannual time span in between periods (not payments) on the timeline? (Answers: 0.625%, 1.8867% and 3.8091%, respectively.) How many period markers would these timelines include? (Answers: 12, 4 and 2, respectively.)

Respectfully,

Brent Pritchard, Member

Boxholm Press, LLC

Brent Pritchard is an author and college finance lecturer with over two decades of industry experience and cofounder of Boxholm Press, LLC, a family-owned-and-operated publishing company providing educational content, products, and services. He pioneers an innovative and approachable new way of learning and teaching the Time Value of Money as well as thought leadership in other business topics. His most recent book is Would Your Boomerang Return? You can contact him on his website here.

Take a Page From the “Finance Textbook Band-Aid” Playbook: Beats a Ban.

If you own it, the finance textbook that is, and you plan to keep it on your desk as a resource like I did back when I was in practice, then consider joining me in this movement against subpar finance content.

If you’re thinking, I’m in, I love your enthusiasm! But you may want to hear me out before joining me in what is currently only my cause as far as I know. There’s a simple step you can take to potentially help people who follow in your footsteps better understand the concept of the Time Value of Money. And you can take this step with your hand! Here goes nothing.

If you come across a page in a traditional finance textbook which misleads you into believing that all interest rates are annual or includes a lowercase of the letter “N” in any building block Time Value of Money equation related to a present value or future value, think about tearing it out! That’s right. Consider defacing that book like it’s nobody’s business, and thereby taking a stand! By tearing out that piece of paper which isn’t worth the paper it’s printed on, traditional publishers might finally come to their senses and change the terminology or variables used. Take a stand with your hand. (That is, unless of course you plan to resell your book or it’s on loan.) In summary, if you own it [your textbook], consider owning it [your education].

Photo by Brent Pritchard.

Here’s an excerpt from my book Would Your Boomerang Return? What Birds, Hurdlers, and Boomerangs Can Teach Us About the Time Value of Money (2023):

This user manual is made possible because of the simplicity related to the TVM Rules, consistency among the improved building block Time Value of Money equations, and connectivity throughout the TVM Formula that culminates in the 3-Step Systematic Approach. You won’t find any superfluous information or terminology in this handbook. Every component or piece has a purpose right down to the letter, literally.

One example of such change is the use of “N” instead of “n” in the building block Time Value of Money equations. The variable “N” represents the number of consecutive periods, or payments for an even annuity, that are subject to the same true investment yield and the same time span in between periods or payments (on the timeline). The investment period may or may not equal the total investment period.

Think back to TVM Rule #2: it’s a Time Value of Money no-no to fail to correspond the time span in between periods or payments (on the timeline) and the time span of the true investment yield.

Thus, “N” is not to be confused with “n” that represents the time span in between periods or payments (on the timeline). It’s “n” that allows you to “tell time” (on the timeline) for a given situation and to ultimately determine the true investment yield for a certain time span. In other words, “n” is in between the period markers on the timeline. The timeline is the visual representation of the total investment period, which will consist of one or more “N’s.”

It’s beyond me why so many other people have failed to recognize this important distinction and—as far as I’m concerned— incorrectly use “n” as a variable in their building block Time Value of Money equations. This shows me they’re loosey-goosey on the whole thing and may have fallen victim to the whole “We do it this way because we’ve always done it this way” line of thought.

I’m not complaining, because it’s improvements like this—not fixes, because nothing is broken—that led me to write this book. My goal is to clear things up and ultimately create the first-of-its-kind user manual for the Mathematics of Finance and the simple “tool” that is the TVM Formula. The formula includes, among other original works, the 3-Step Systematic Approach for applying the Mathematics of Finance to analyze and evaluate real-world Time Value of Money situations.

If considered in isolation, it might not appear that the use of “N” in the building block Time Value of Money equations is a change worthy of being called an improvement; however, the value of the user manual is in the whole rather than the sum of its parts.

In traditional textbooks, the use of the notation “n” in one or more of the building block Time Value of Money equations is widespread. In all fairness, I can kind of see why other people might choose to use “n” in their building block Time Value of Money equations. This may be too forgiving, but I would like to think that these other people are thinking that using the variable “n” instead of “N” makes sense because there are going to be times when there is only one “n” in an investment period or because the summation of multiple “n’s”—the number of periods (on the timeline)—won’t always equal the total investment period. I get it, but the improved definition of “N” recognizes this.

Recall that the variable “N” represents the number of consecutive periods, or payments for an even annuity, that are subject to the same true investment yield and the same time span in between periods or payments (on the timeline). There’s not even a direct reference to an investment period let alone the total investment period. Sometimes “N” will equal the total investment period. Sometimes it won’t. Sometimes “n” will equal “N,” but those instances will be few and far between. The definition of “N” has both these potential arguments covered.

Frankly, other people’s use of “n” in their building block Time Value of Money equations is probably more a result of there not having been a definitive systematic approach in print. But that’s changed with the publication of this handbook!

Another benefit that can’t be overstated is how separating “n” from “N” gets people focused on making sure to correspond the time span in between periods or payments (on the timeline) (n) and the time span of the true investment yield (i).

Another variable that you have likely encountered for building block Time Value of Money equations and the primary TVM financial calculator inputs in many traditional textbooks is “r” or “i” for the true investment yield. At first, one might think that this is not that big of a deal. But it’s a really big deal when one of the objectives is to eliminate ambiguity and create agreement by making all the pieces fit together.

For reasons that will become clear as you flip the pages of this book, I landed on the letter “i” to represent the true investment yield for more than the fact that i is the first letter of “investment” or “investment yield.” I took the liberty of eliminating the “r” variable.

In the building block True Investment Yield equation, the simple investment yield is denoted by “s.” The “s” variable remains. But since the true investment yield is—get it, “i” and “s”—what it’s all about when it comes to the Time Value of Money, your focus will be on the “i” variable.

You may find yourself rewriting other authors’ variables related to the building block Time Value of Money equations or primary TVM financial calculator inputs to make them jibe with the TVM Formula and the original 3-Step Systematic Approach, which are presented in this book. That’s OK, but the other way around won’t fly.

If you think I’m blowing this out of proportion, I’ve seen authors define “n” in their building block Time Value of Money equations as, “the number of years” and, “m” as “the number of compounding periods within a year.” See what’s wrong with this?

It is misguided to think that periods or payments (on the timeline) will always be annual. Again, I think the main culprit for why other people choose to settle for using a variable other than “N” is that they are lacking a definitive systematic approach. But just using “N” doesn’t solve the bigger problem! There’s more to it than that, which is where simplicity, consistency, and connectivity come in, and why a formula, the TVM Formula, needed to be developed. In the 3-Step Systematic Approach presented herein, you’ll be calculating the true investment yield as your “warm up” before “working out” the math. The TVM Formula, which allows you to apply the Mathematics of Finance to analyze and evaluate real-world Time Value of Money situations using the 3-Step Systematic Approach, is a one-size-fits-all tool.

Why not turn the torn out page(s) in to your finance instructor? (And if it’s helped you, I’d be honored if you would recommend that they consider using the “Boomerang book” as required or supplemental material to help finance students finally understand the Time Value of Money like the backs of their hands. The Boomerang book was written for you: whether you’re an aspiring or current finance professional or finance educator.)

Brent Pritchard is an author and college finance lecturer with over two decades of industry experience and cofounder of Boxholm Press, LLC, a family-owned-and-operated publishing company providing educational content, products, and services. He pioneers an innovative and approachable new way of learning and teaching the Time Value of Money as well as thought leadership in other business topics. His most recent book is Would Your Boomerang Return? You can contact him on his website here.

Get the Book Today!

Would Your Boomerang Return? provides a fun, new take on how the Mathematics of Finance is learned and taught:

All-in-one resource: all the important information on this all-important topic in one place with chapters in the What and How sections that double as individual lessons

Ease of reference: includes the first-of-its-kind user manual for the Mathematics of Finance with chapters named after sections typically found in an actual user manual for quick look up

Simple and definitive tool: 3-Step Systematic Approach for analyzing and evaluating real-world Time Value of Money situations

Decision-making framework: 23 real-world Time Value of Money questions, space to work out answers, and a "baseball count" system to evaluate understanding of the different types of questions

An easy read: complete with sprinklings of real-life stories and maybe even an ounce of inspiration here and there

Sign up for TVM 2$days, a weekly blog that offers a fun, new take on this age-old topic and financial education insights from Brent Pritchard.